HardMoneySearch Guide

Hard Money Loan Rates: What to Expect in 2026

Introduction

Hard money loan pricing combines an annual interest rate with upfront origination points. Both vary significantly by lender, property type, borrower experience, and local market competition — making direct comparison across multiple lenders the only reliable way to understand your actual project cost.

Hard money serves investors needing rapid closings or non-conventional loan structures. Fix-and-flip buyers acquire and renovate properties for resale. Bridge borrowers need interim financing between property transitions. DSCR investors want rental income evaluation rather than W-2 verification.

National averages provide context, not actual quotes. Your terms depend on lender specialization, experience level, and property specifics. Construction-focused lenders price differently than rental portfolio specialists. Credit profile, liquidity, and exit strategy all influence final pricing.

Regional market conditions create pricing variations across metropolitan areas. Coastal markets with higher property values often see more competitive rates. Secondary markets may command premium pricing due to limited lender options.

How Rates Are Structured

Rates, points, loan-to-value limits, ARV limits, fees, and days-to-close are informational ranges only when sourced. They are not guarantees, quotes, commitments to lend, or financial advice. Actual terms vary by lender, borrower qualifications, property type, leverage, location, and underwriting review.

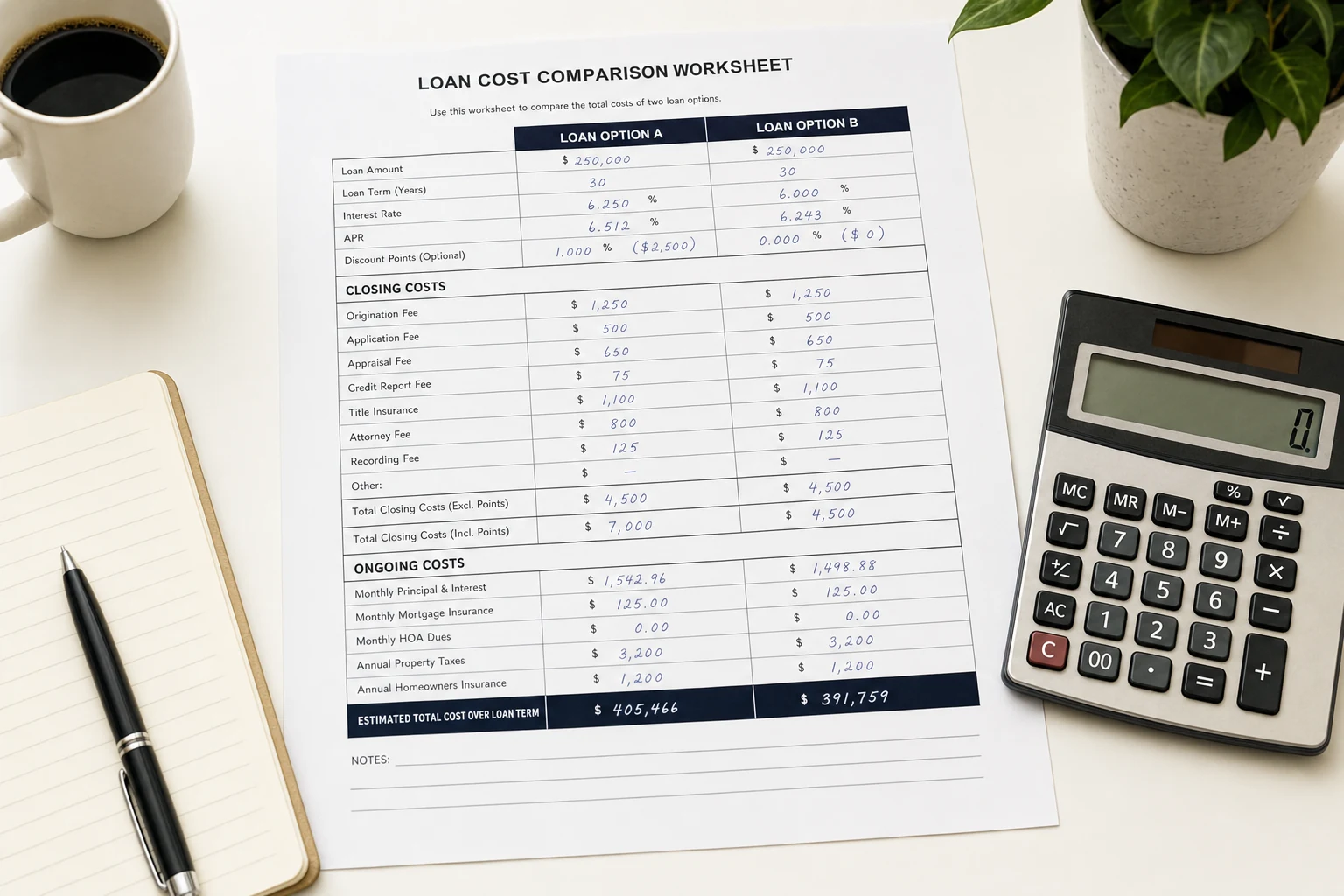

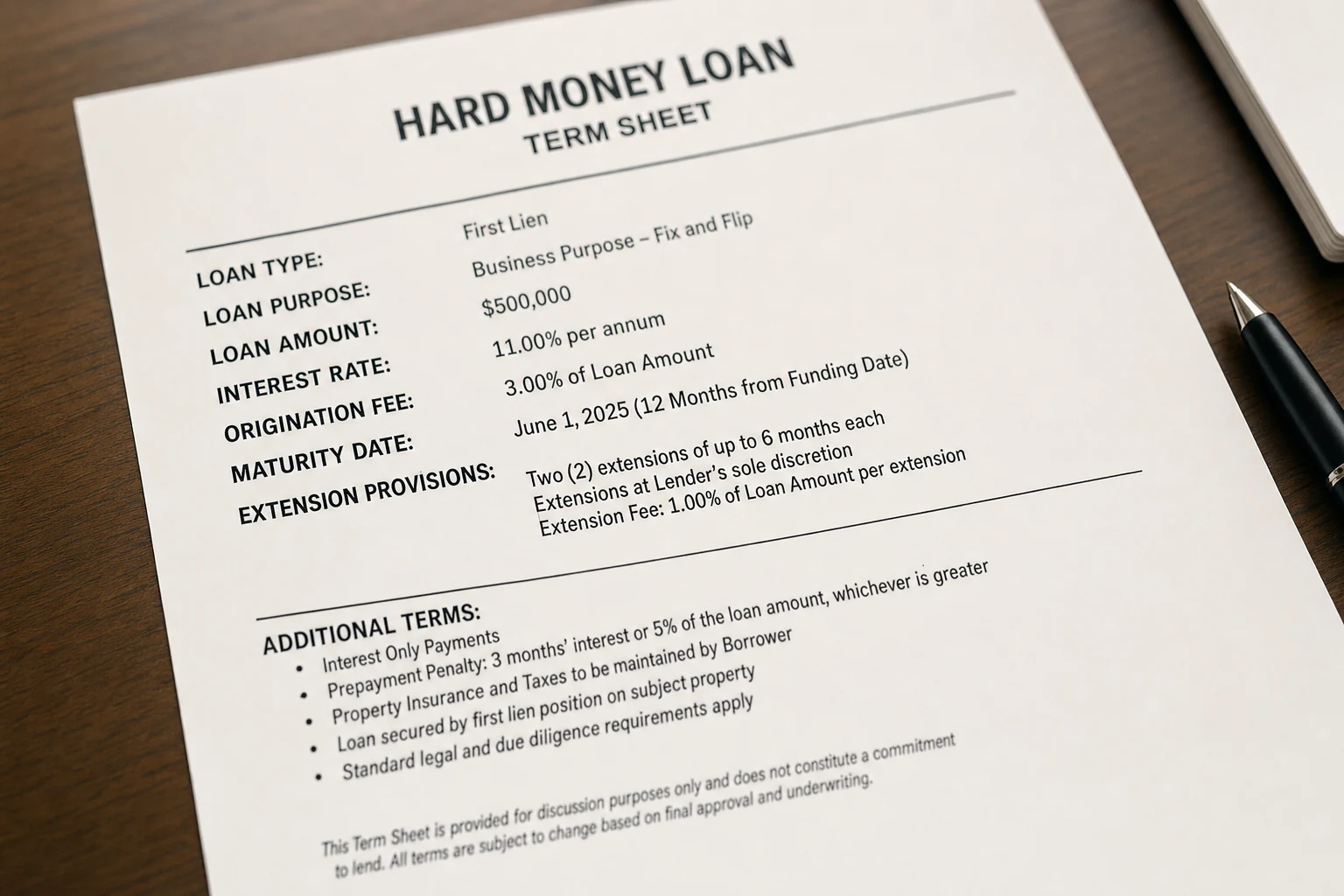

Hard money pricing combines interest rates and origination points. Interest rates represent annual borrowing cost, charged monthly on outstanding balances. Points equal upfront fees calculated as loan amount percentages, paid at closing.

Additional fees impact total project costs beyond base pricing. Appraisal fees range from $400 to $1,200 depending on property complexity. Processing fees, underwriting charges, and documentation costs add upfront expenses. Some lenders charge application fees while others build costs into points.

Term length affects both pricing structure and total expense. Six-month terms typically carry different rate-point combinations than 18-month loans. Shorter terms often feature lower rates with higher points. Longer terms may reduce points but increase interest expense over time.

Lenders offer various rate-point combinations for identical loan amounts. Higher points with lower rates suit longer hold periods. Lower points with higher rates work for rapid turnover projects. Monthly payment obligations shift significantly based on these choices.

Construction projects requiring draw schedules and inspection coordination often command different pricing than simple purchase-bridge scenarios. Each lender's fee structure reflects their operational complexity and risk assessment methodology.

Exit fee policies vary among lenders. Some charge prepayment penalties within the first 90 days. Others allow prepayment without penalty after interest reserves are met. Document recording fees, wire transfer charges, and legal review costs can add $1,500 to $3,000 to closing expenses.

*Rates, points, and fees shown are illustrative ranges that vary by lender and borrower qualifications.*

What Drives Pricing

Property type significantly influences pricing across lenders. Single-family rehab projects generally receive more competitive terms than mixed-use commercial properties. Ground-up construction carries additional costs for draw management and timeline risks that standard bridge lenders avoid. Borrower experience creates substantial pricing variations. Documented fix-and-flip history or rental property management background often secures better terms than first-time investor applications. Each lender weighs experience differently based on their underwriting priorities and risk tolerance. Lender specialization drives market pricing differences. Companies focused exclusively on short-term flips price aggressively within that niche. Complex construction draw specialists or commercial bridge experts charge premium rates for specialized knowledge and operational complexity. Speed requirements create significant cost tradeoffs throughout the market. Ten-day closings typically cost more than 30-day timelines. Emergency bridge financing or competitive acquisition scenarios justify premium pricing when conventional financing cannot meet deadlines. Geographic focus affects lender competitiveness. Regional companies may offer aggressive pricing within their core markets while national lenders provide consistent terms across multiple states. Local market knowledge and operational efficiency influence pricing strategies. Project complexity beyond standard rehab work commands higher rates. Historic properties, environmental issues, or unusual zoning situations require additional due diligence and specialized expertise that impacts lender costs. Loan-to-value ratios create pricing tiers within lender programs. For illustration only, conservative 60% LTV deals often qualify for base rates. This figure is illustrative only, not a quote or guarantee. For illustration only, higher leverage at 75% to 80% LTV typically adds premium pricing. This figure is illustrative only, not a quote or guarantee. Maximum leverage varies by property type and borrower qualifications. Seasonal market conditions influence pricing cycles. Spring and summer demand peaks may tighten availability and increase rates. Winter periods often provide more favorable terms as competition for deals decreases among investors.

Points vs Rate: How to Compare

Calculate total borrowing cost across your entire hold period rather than comparing monthly payments alone. Different rate-point combinations create varying economics over time. Consider this scenario for illustration: A $300,000 loan at 10% with 3 points costs $9,000 upfront plus $2,500 monthly interest (rates vary by lender). For illustration only, the same loan at 12% with 1 point costs $3,000 upfront plus $3,000 monthly. This figure is illustrative only, not a quote or guarantee.

Over six months, the first option totals $24,000 versus $21,000 for the second. Extend the timeline and economics shift. For illustration only, over 12 months, the 10% option costs $39,000 total while the 12% loan costs $39,000. This figure is illustrative only, not a quote or guarantee. The break-even occurs around one year of borrowing.

Total cost calculations must include all fees beyond rate and points. Processing charges, appraisal costs, and potential extension fees affect project profitability. Monthly carrying costs vary significantly based on rate-point combinations and actual hold periods.

Extension fee structures become critical for projects with timing uncertainty. Some lenders charge additional points for renewals while others increase interest rates. Include prepayment scenarios in your comparison since early payoff eliminates future interest expense.

Focus on total borrowing expense rather than individual components when evaluating offers from multiple lenders. Create spreadsheet models showing various hold period scenarios. Factor in realistic project timelines based on scope complexity and local approval processes.

Interest-only payment structures simplify monthly cash flow planning compared to principal-and-interest amortization. Most hard money loans operate on interest-only terms with balloon payments at maturity. This structure concentrates borrowing costs into points and interest rather than principal reduction.

Compare annual percentage rate calculations when available, as these include points and fees in standardized format. However, APR assumes full-term borrowing while most hard money projects close early.

Extension Fees and What Happens When Projects Run Long

Extension fee policies become critical when projects exceed original terms. For illustration only, a lender charging 1% to 3% monthly extension fees could add 3% to 9% to total project cost on a six-month loan that runs three months over. This figure is illustrative only, not a quote or guarantee. Construction and major rehab projects face the highest extension risks. Permit delays, weather interruptions, contractor conflicts, and material shortages routinely exceed initial timelines. Four-month renovations can stretch to eight months when multiple trades fall behind schedule. Extension structures vary significantly between lenders. Some offer automatic renewals with preset terms. Others require new underwriting, updated appraisals, or approval processes adding weeks to resolution time. Fees may compound while borrowers wait for extension approval. Conservative timeline planning becomes essential given these fee structures. Experienced borrowers often secure longer initial terms than base estimates suggest, accepting higher monthly costs to avoid extension penalties. Others negotiate capped fees or graduated pricing during initial discussions. Municipal approvals, historic properties, and complex rehabilitation requiring specialized trades create the highest timing risks. Environmental issues, zoning complications, or structural surprises can derail even conservative schedules. Extension costs transform profitable projects into marginal ones. Budget planning should account for potential delays, especially on projects involving government approvals or extensive renovation scope beyond cosmetic improvements. Build contingency reserves covering three to six months of additional carrying costs including extension fees. For illustration only, default interest rates during extension periods may be 2% to 5% above base rates. This figure is illustrative only, not a quote or guarantee. Some lenders waive extension fees for borrowers with strong payment history and clear project progress documentation. Negotiate extension terms during initial loan discussions rather than waiting for deadline pressure. Establish automatic renewal triggers, fee caps, or graduated pricing structures. Document these agreements in writing as part of original loan terms.

What to Ask Before You Sign

Demand total cost breakdown including all fees, points, and extension charges in writing. Confirm prepayment options and early payment penalties. For construction projects, clarify draw schedules and inspection requirements. Request specific funding timelines and closing conditions that could cause delays. Verify lender licensing and complaint history through state regulatory databases. Confirm loan servicing arrangements and payment processing procedures. Document all verbal promises in written loan agreements before signing. Contact Denver-based lenders at Denver hard money lenders or Houston specialists through Houston hard money lenders. Additional guidance available at how to choose a hard money lender. *HardMoneySearch.com provides educational information only. We are not lenders.

Additional resources: https://www.nmlsconsumeraccess.org/.